Why a Hard Market Causes Rate Increases

In the past few weeks, I handled several medical malpractice renewals in which pricing was to go up substantially. The primary reasons stem from current and projected claim activity and the fact that we are in a “hard market.”

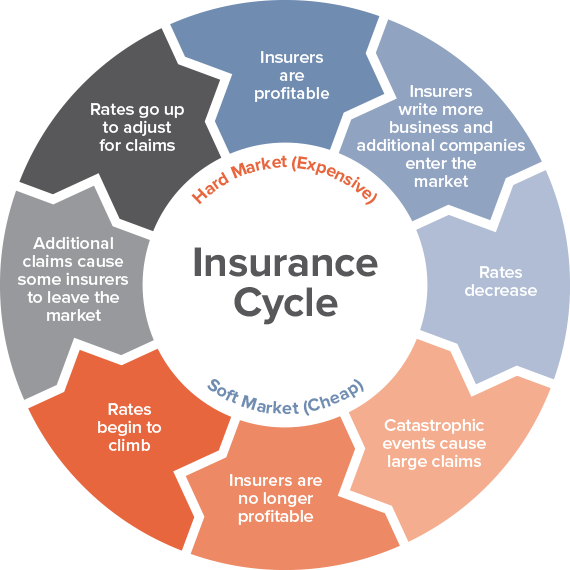

As Insurance Business Magazine points out, “a hard market is the upswing in a market cycle, when premiums increase and capacity for most types of insurance decreases.” In contrast, a soft market “is characterized by low rates, high limits, flexible contracts, and high availability of coverage.”

The insurance market is cyclical, rotating through soft and hard market periods over time. The following figure illustrates some of the typical factors that cause soft and hard market patterns.

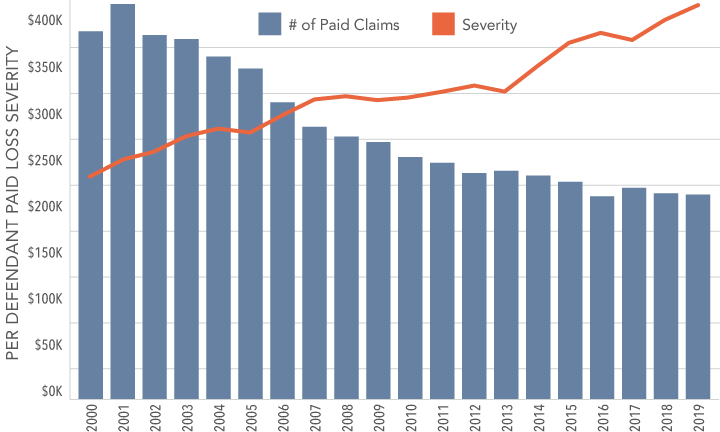

Larger and more severe claims in recent years are taking a toll now. As the number of claims overall has gradually lowered and leveled off since 2001, the severity of these clams has steadily risen, which is a hard market influencing factor. We can see this clearly as indicated by the red line in the bar graph below.

To summarize, you will typically find these conditions during a hard market:

- Increases in the frequency and/or severity of claims

- Fewer insurance companies in the market

- More burdensome regulations on insurers

- Lower investment returns for insurers

- Stricter underwriting and reduced coverage

- Higher premiums

Fortunately for my clients in the cases mentioned above, I was able to help. In one situation, I negotiated premium credits for a group of physicians. In another case, I am moving the policy to a different company that’s willing to reduce their pricing without compromising coverage.

Why the Hard Market Now?

We know that Covid-19 is playing a role this time around due to future claims’ unpredictability. As earlier indicated, the severity of claims is way up and continues trending that way. Societal conditions leading to more lawsuits are causing higher losses and claims among insureds. Increasingly proactive litigation leads to higher and higher settlements. Resources at national and state levels have been redirected like never before, and insurance companies are concerned, causing their underwriters to cautiously choose the risks they will insure.

The year 2020 posed additional challenges including:

- Property & Casualty net income after taxes dropped 27.5% in the first nine months of 2020.1

- 19 Natural Disaster Events occurred in 2020 with over one billion in direct losses1

- Insurers are bracing for Covid-19 related claims.2

Medical malpractice insurance is particularly troublesome because of the uncertainty of Covid-19 related claims. We see the potential of “Failure to Diagnose” claims because patients could not see their doctors and delayed diagnostic testing. Looking back further, we see standard insurance companies losing business as healthcare providers join healthcare systems that provide insurance through a captive. These unfortunate events leave fewer doctors for traditional carriers to insure which leads to reduced volume, lower profitability and rate increases.

How Can You Protect Yourself During The Hard Market Cycle?

Despite the hard market, there are still differences between carriers. Knowing who’s who and what’s what in coverages and costs goes a long way to mitigating the impact of malpractice insurance premium hikes. For example, doctors can earn premium credits for applying best practices, and we find savings for many by discovering they are already eligible for significant discounts.

Focus on Finding the Best Options

While we agents have no control over broad market conditions affecting premiums, we, who are willing, can do the research, the “shopping,” and the negotiation to find the absolute best coverage at the lowest cost available. That has always been a big part of our work at Perron Insurance because it’s one of the most effective ways to help protect physicians’ practices and income.

What does this mean for you?

For your upcoming renewal, I recommend starting the process early to obtain the best outcome. Research and analysis based on your specific needs are the key to success. I would be honored to review your coverage and offer recommendations to lower your premiums and avoid a hard market hit on your insurance costs.

I have over twenty years of experience specializing in obtaining optimal and affordable malpractice insurance for physicians to protect their assets and income.

Feel free to call me at (603) 926-1318 or send me an email so I can learn about you and your practice’s specific needs.

1. Turner H. Property & casualty industry income plummeted in 2020 | PropertyCasualty360. Property & Casualty 360. https://www.propertycasualty360.com/2021/02/18/property-casualty-industry-income-plummeted-in-2020/?slreturn=20210212124214. Published February 18, 2021. Accessed March 12, 2021.

2. COVID-19 Impact to Property & Casualty Insurance | Deloitte US. Deloitte. https://www2.deloitte.com/us/en/pages/financial-services/articles/covid-19-impact-to-property-casualty-insurance.html. Accessed March 12, 2021.